The Macro Landscape: What’s Driving Market Conditions?

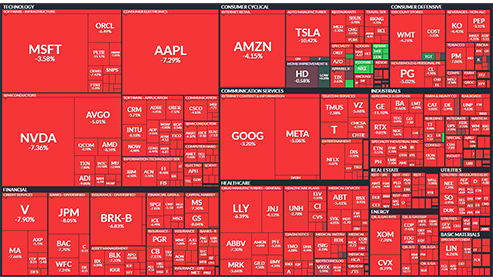

The market’s relentless climb continued today as the S&P 500 notched another record high, closing at 6,144.15. The Dow Jones followed suit, rising to 44,627.59, while the Nasdaq edged up to 20,056.25. But beneath the bullish headlines, significant macroeconomic shifts are at play.

The Federal Reserve’s latest meeting minutes revealed policymakers are still concerned about inflation and external risks, notably tariffs and geopolitical instability. Additionally, President Trump’s announcement of a 25% tariff on autos, semiconductors, and pharmaceuticals raised fears about potential supply chain disruptions and inflationary pressures. The market, however, appears to be interpreting this as a negotiation tactic rather than an immediate economic threat.

Zooming In: How This Impacts the Market

With interest rates holding steady but inflation concerns lingering, equity markets are balancing between optimism and caution. Historically, aggressive tariff policies have caused volatility, as companies reprice supply chain risks and consumers brace for higher costs.

The tech sector saw some divergence today. While Microsoft rose 1.3% after announcing its quantum computing advancements, the broader semiconductor sector faces uncertainty due to tariff concerns. Analog Devices (ADI) surged 9.7% on strong earnings, but the broader industry remains vulnerable to policy changes.

In the auto sector, Tesla saw a 1.8% gain, despite the tariffs directly impacting the industry. However, Nikola faced a crushing 39.1% decline after filing for bankruptcy protection, highlighting the risks for smaller players in capital-intensive industries.

Key Risks & Opportunities for Traders

Risks:

-

Prolonged tariff tensions could elevate input costs for manufacturers, squeezing profit margins.

-

Inflationary pressures may keep the Fed hesitant to cut rates, limiting further equity upside.

-

Weakness in the housing market (January housing starts down 9.8%) may signal broader economic softness.

Opportunities:

-

Short-term bullish momentum remains, especially in sectors less affected by tariffs, such as AI and cloud computing.

-

Options traders may find opportunities in semiconductor volatility, with put spreads on chipmakers vulnerable to trade restrictions.

-

The bond market, with 10-year Treasury yields at 4.53%, suggests a flight to safety is brewing—indicating potential hedging opportunities in gold and defensive stocks.

Trading Strategies: How to Play This Thesis

For traders looking to capitalize on the current macro environment:

-

For bullish investors: Consider tech and AI plays like Microsoft (MSFT) and Nvidia (NVDA), both benefiting from continued demand and innovation.

-

For bearish traders: Watch for put spreads on overextended semiconductors like AMD and Qualcomm, particularly if tariff negotiations turn hostile.

-

For income-focused strategies: Bond yields are stabilizing, making covered calls on defensive dividend stocks a strong play.

The Trader’s Take

Markets may be rallying, but traders must be cautious. While optimism around AI and tech continues, economic realities like tariffs, inflation, and housing weakness could introduce turbulence in the months ahead. The key is to stay ahead of the macro narrative—trade with the trend, but keep a defensive hedge in place.

MSFT NVDA AMD QCOM